What Am I seeing on my Portfolio X-Ray on the portal?

Dominic Thomas

March 2026 • 3 min read

What Am I seeing on my Portfolio X-Ray on the portal?

One of the features of our secure portal is the ability to see the live valuations of your investments. These are not ‘held’ on our portal, it is merely a secure reporting tool, loaded with data pulled from the original sources (ie investment platforms, such as Fundment, Nucleus, 7IM, Transact and so on).

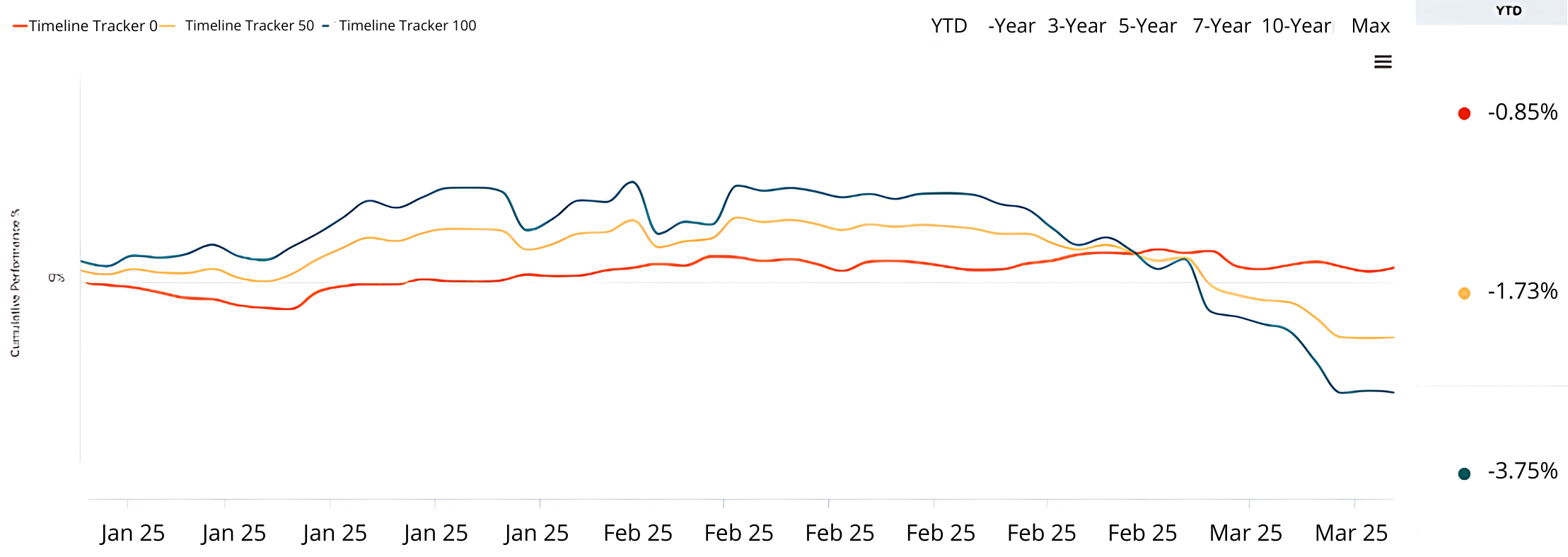

The portal pulls through current holdings and allocations, but doesn’t do a particularly good job of showing historic ones. You will see previous valuations, which reflect your actual valuations, but not of a fund that you didn’t have say three years ago but do today due to changes we may have made.

When you review this, you will see a combination of holdings and funds. You have a globally diversified portfolio of assets that are either shares in companies around the world or are a form of loan (debt) that a Government or company have issued. In the latter case (Bonds, Gilts and Cash) you lend your money to Governments and Companies on the agreement that they return it at a set date and in the meantime provide a fixed (agreed) level of interest. It’s more sophisticated than this implies, but essentially that’s what is happening underneath. So you hold lots (7,000-30,000) of securities within funds within your portfolio at a very low cost.

Your portfolio is based in part on your responses to loss (nobody likes it, but we all respond differently). In essence how much panic you feel. Unfortunately, whilst I would prefer emotions were removed from investing, they are a default setting on humans, so the attitude to risk questionnaire helps us assess how anxious you get seeing a large fall in value (or a small one). I am not a robot, but the world stock markets are not the place to develop your character. However, clearly part of good financial planning is to set an appropriate level of risk to generate returns that will beat inflation (and keep your spending power favourable) within the context of our conversations and what the money represents to and for you.

This is given more context by how long you are investing (for most clients it’s the remainder of their lifetime) and the level of average annualised returns that you need to achieve to provide the lifestyle and financial security that you require. These are obviously unique to you and your circumstances. The more held in shares the greater the long-term returns, but the greater the volatility (valuation wobbles).

Then there is possibly some short-term opinion on the state of the global economy or your need for cash (or both) which may also temporarily influence our selection.

The portfolio contents changed recently (to reduce costs and further increase diversification). So these funds are the current position not what you actually held three years ago. Secondly we may have taken some steps (with your agreement) to shore things up based on your short-term requirements for capital or income.

We use data and attempt to extract from this the evidence rationale for making decisions. The mix is appropriate and will include underperformers sometimes. You may remember me showing you an image that looks rather like a patchwork quilt of top performing assets or markets in each calendar year – a brightly coloured image. It’s very human to attempt to find patterns, but the pattern is that there is no pattern. Here is a recent one by Dimensional, you don’t need to worry about the small print on this, it’s the concept that is important. Ask me if you want a readable copy.

We combine assets to attempt to deliver a particular long-term return. Think of making something with flour, eggs, salt, sugar etc… different quantities and cooking methods provide anything from a pancake to a souffle (and a whole lot besides).

Not all elements will always ‘win’ or even be positive, but they add to the mix to deliver the required result. Think of it a bit like buying umbrellas for rain along with sunglasses and suntan lotion for sunshine. Markets are cyclical and random. In short we don’t look for the needle in the haystack, we buy the haystack.

Sorry for all the metaphors, but I think they work! To assess historic performance, you are better doing this in your platform portfolio (Fundment etc) or leaving it to us and do something less boring instead… (ok you have to be a certain age to get the Why Don’t You? Reference).

Does that make sense?

You may find this a helpful aid in thinking about your investments: