The Deep End

The Deep End

Have you ever seen a child standing tentatively at the edge of a swimming pool? She’s torn between her desire to join the gang in the water and her fear of diving in. In committing to the market, investors can be like that.

You can always find a reason for not investing. “Perhaps I should wait till after interest rates rise?” goes one line of the thinking. “Or maybe I should delay till there’s more clarity on China? Or hold back until after earnings season?”

Emotions and assumptions usually underlay this indecision. The emotion can be anxiety about “making a mistake” or fear of committing at “the wrong time” and suffering regret. The assumption is that there is a perfect time to invest.

Obviously, the ideal solution would be to enter the market just as it bottoms and exit the market right at the top.

But the reality is that precisely timing your exit and entry is close to impossible. If it were easy, millions would be doing it and getting very rich in the process. Instead, the only ones who tend to consistently make money out of market timing are those who write books about it.

The financial media certainly love market timing stories. For one thing, there is always some event or variable they can peg it to—like a decision on interest rates or upcoming earnings or a chart indicator. For another, the idea of timing the market is a powerful one and tends to get readers’ attention.

For example, one high-profile US forecaster in early 2012 predicted a 50-70% equity market decline over the following two-to-three years. It was to be a replay of the 2008-09 crisis, he said, but with an even deeper recession.1

Timing the market… or time in the market?

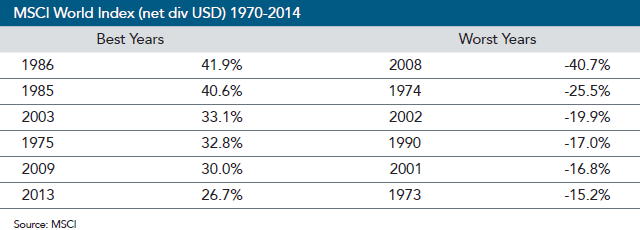

That turned out to be a bad call. Global equity markets, as measured by the MSCI World Index, delivered a total positive return in Australian dollars of 93% from the end of 2011 to the end of 2014.2 In USD, it was 53%.

Others advocate more elaborate timing strategies. For instance, one recent academic paper suggested the stock market delivers better returns relative to Treasury bills in the second, fourth and sixth week after each of the US Federal Reserve’s policy-setting meetings in a given year.3

The idea here is that the Fed leaks information about its interest rate intentions in such a predictable way that, even without the information, savvy investors can make money by just buying stocks in certain periods.

While these theories can be fascinating, it is arguable how many of us have either the time or inclination to try them out. And even if we did, this does not take account of the costs of all the required trades or the possibility that as soon as we implemented the idea it would be arbitraged away.

So ahead of a central bank meeting, some would-be investors fret about whether they should hold off until they see how the market reacts. Others already invested worry whether they should take their money out.

What really matters

The truth is that for long-term investors, these issues should be irrelevant. What matters is how their portfolios are structured and how they are tracking relative to their chosen goals. Markets will go up and down, security prices will change on news and it makes little sense to second guess them.

But while no one yet has come up with a consistently successful strategy for timing the market to perfection, there are some things that everyone can do to help ease the anxiety they feel about investing.

One is to realise that it does not have to be a choice between being 100% in the market and 100% outside. Ideally, an investor should stick to their strategic asset allocation—be it 70/30 or 60/40 or 50/50 equity/bonds.

Another is that this strategic allocation can be combined with periodic, disciplined rebalancing, in which the investor shifts assets from well performing asset classes to those less favoured. This is a good way of controlling risk without necessarily trying to time the market.

A third option is that there is nothing wrong with investors taking into account the returns they have already enjoyed and adjusting their asset allocations if they are on course to meet their goals. So, for example, for some investors it might make perfect sense to lock in returns after a good period and put the money into short-term fixed income if that meets their needs.

Yet another option is dollar-cost averaging. This is a method where an individual invests small amounts of an available pool of cash into the market over a period, rather than investing a lump sum in one go.

A useful contribution on this subject comes from Ken French, Professor of Finance at the Tuck School of Business at Dartmouth College. In his role as an academic, Professor French says the optimal decision is to invest it all at once. But while this might give an individual the best investment outcome, he says it might not be the best investment experience.4

This is because people tend to feel regret more strongly when it results from things they did do than from things they did not. So, for instance, it feels much more painful to buy stocks now and see the price go down than it is to neglect to buy stocks and the price goes up.

Professor French says that by dollar cost averaging, people can diversify their “acts of commission” (the stuff they did do) as opposed to their “acts of omission” (the stuff they didn’t do).

“The nice thing is that even if I put my finance professor hat back on, it’s really not that damaging to your long-term portfolio to just spread it out over three or four months,” he says. “So if you as an investor find that’s much more tolerable for you, you’re not really doing much harm.”

So, in summary, it’s always difficult to choose exactly the right time to get into or out of the market. For instance, it would have been nice to get out in late 2007 and back in around early March 2009.

But most mortals are unable to finesse it to that degree. The good news is that there are other options than just staying out of the market altogether and plunging back in.

These include maintaining a long-term strategic asset allocation in the first place, periodically rebalancing, taking money off the table if retirement goals are on track and dollar-cost averaging if that provides comfort.

The underlying philosophy in all these options is that individual investors are making decisions based on their own needs and risk appetites, not according to someone else’s opinion as to what the market does next.

Uncertainty will always be an integral part of investment (and life). But there are many things we can control. And this is where a good adviser comes in.

1. “Get Set for a Crash, Forecaster Says”, Globe and Mail, 10 January 2012

2. MSCI World Index (net div, AUD), Returns Program

3. “Want to Play the Market? Count the Fed Leak Weeks: Study”, Reuters 21 November, 2015

4. Fama/French Forum, “Dollar Cost Averaging”, 23 June, 2009

Jim Parker

Vice President, Dimensional

You can read more articles about Pensions, Wealth Management, Retirement, Investments, Financial Planning and Estate Planning on my blog which gets updated every week. If you would like to talk to me about your personal wealth planning and how we can make you stay wealthier for longer then please get in touch by calling 08000 736 273 or email [email protected]